Finding the right small business loan can be complicated, with numerous options, rules, and requirements to consider. Whether you’re launching a startup, expanding operations, or covering day-to-day expenses, understanding how loans work is essential for making informed choices.

This blog brings together the most frequently asked questions by business owners about financing, covering topics such as eligibility, applications, loan types, SBA programs, repayment, and more.

Use this FAQs blog to guide your funding options and choose the one that best fits your business needs.

General Eligibility & Basics

Small business loans vary in terms of eligibility, required documents, and collateral, making it essential to understand the specific requirements of each option.

1. Who qualifies for a small business loan?

Small businesses with steady revenue, a business plan, and decent credit may qualify. Lenders typically review income, time in business, credit history, and ability to repay. Some programs are available even if your business is new, especially SBA loans or microloans tailored for smaller operations.

2. Can individuals or sole proprietors apply for small business loans?

Yes. Sole proprietors and individuals running a registered business can apply. Lenders typically consider personal credit scores, business revenue, and cash flow when evaluating loan applications. Since the company isn’t legally separate, your personal financial history plays a significant role in qualifying and determining loan terms.

3. What documents are required when applying for a small business loan?

Most lenders require financial statements, recent tax returns, bank statements, business licenses, and a comprehensive business plan. Some may also require proof of collateral, legal documents, or ownership details. Having organized records helps speed up the approval process and improves your chances of securing favorable terms.

4. Do startups or newly established businesses qualify for small business loans?

Yes, but it can be more challenging. Startups often lack a long financial history, so lenders may require strong personal credit, collateral, or a detailed business plan to mitigate risk. SBA microloans, grants, or alternative online lenders are suitable options for newer businesses that need smaller amounts of funding.

5. What is the difference between secured and unsecured small business loans?

Secured loans require collateral, such as equipment, property, or accounts receivable, which reduces risk for lenders and often results in better rates. Unsecured loans don’t require collateral but usually need strong credit and carry higher interest rates. Each option has trade-offs depending on your business’s financial situation.

6. What is a collateralized small business loan, and what assets can be used?

A collateral small business loan is backed by business or personal assets, which reduces risk for lenders. Collateral may include vehicles, equipment, or inventory. If repayment fails, the lender may claim the asset as collateral. These loans usually offer lower rates and higher borrowing limits.

People often ask who qualifies, what’s required, and how the process works, so let’s clarify that.

Application Process

Wondering how to apply, what paperwork is required, and how long approvals take? Here’s what you should know.

7. Can I apply for a small business loan online?

Yes, most lenders and fintech platforms allow online applications. You’ll typically complete a form, upload documents, and receive a decision more quickly than with traditional banks. Online applications are convenient, though requirements remain the same; credit history, revenue, and business information still guide the lender’s decision.

8. Do I need to have a business account with the lender to apply for financing?

Not always. Some banks prefer or require applicants to maintain a business account with them, but many lenders don’t. Having an account may simplify approval and fund transfers, but it’s not a universal rule. Always check your lender’s eligibility criteria before submitting your application.

9. How long does it take to get approved for a small business loan?

Approval times vary. Online lenders may provide same-day or next-day decisions, whereas traditional banks and SBA loans can take several weeks to process. Factors include loan size, documentation, and credit history. Generally, expect a timeframe of anywhere from a few days to several weeks, depending on the type of loan.

10. How quickly can I access funds after my loan is approved?

Funding speed depends on the lender and loan type. Online lenders often disburse funds within one to three business days. Banks and SBA loans may take longer, sometimes several weeks. Having complete documents and a business bank account can help expedite the funding process.

11. Are there state-specific programs, like small business loans in Florida, Arizona, or Indiana?

Yes. Many states offer tailored programs, including small business loans that Florida entrepreneurs can access through development agencies, state-backed funds, or community banks. Similar opportunities exist in Arizona and Indiana. These programs aim to support local businesses with flexible terms and lower interest rates.

Once you understand how to apply for and access funds, the next step is exploring the different loan types and how each one can be used to support your business.

Loan Types & Uses

Small business loans come in different forms, and the right choice depends on your specific needs and situation.

12. What types of small business loans are available?

Common loan types include term loans, SBA loans, business lines of credit, equipment financing, invoice factoring, and merchant cash advances. Each serves a different need: term loans for significant expenses, lines of credit for flexible cash flow, SBA loans for lower rates, and equipment loans for asset purchases. Some business owners also compare loans with other investment options, such as a mutual fund, to determine which one best fits their financial goals.

13. What are unsecured small business loans, and who should consider them?

Unsecured small business loans don’t require collateral. They’re best for businesses with strong credit and steady revenue but limited assets to pledge. While faster to obtain, they often carry higher interest rates. They help cover short-term expenses, payroll, or growth opportunities when collateral isn’t available.

14. Can I get small business loans for restaurants?

Yes. Many lenders and SBA programs offer small business loans for restaurants. Funds can cover startup costs, renovations, equipment, or working capital. Since restaurants are seen as higher risk, strong financial records or collateral may improve approval chances. Specialized restaurant loan programs may also be available in your local area.

15. Are there small business loans designed for veterans?

Yes. Many programs offer small business loans for veterans through SBA initiatives, such as Veterans Advantage, as well as state-backed options. These often offer reduced fees, flexible terms, or easier qualification requirements. Nonprofit and community lenders also support veteran-owned businesses, giving access to funding that helps them grow and succeed.

16. What are small business payroll loans, and how do they work?

Payroll loans provide short-term funding to cover employee wages and benefits. They help businesses manage cash flow during seasonal dips or delayed payments. Repayment terms are usually short, and interest rates can vary. They’re meant as a bridge to ensure staff are paid on time.

17. What are small business auto loans, and what vehicles qualify?

Small business auto loans finance vehicles used for business purposes, such as vans, trucks, or service cars. The vehicle usually serves as collateral. Lenders may require proof that the vehicle is for business use. Loan terms depend on credit, business revenue, and the type of vehicle financed.

18. Can small business loans be used to purchase or refinance commercial real estate?

Yes. Many banks and SBA programs allow small business loans for real estate purchases, expansions, or refinancing. SBA 504 and 7(a) loans are popular options for this purpose. These loans usually require collateral and longer repayment terms, making them suitable for property investments.

19. Can agricultural businesses qualify for small business loans?

In many cases, farms and agricultural businesses often qualify for small business loans, though requirements may vary. In addition to SBA programs, the USDA offers farm-focused loan options. Funds can be used for equipment, land, or operating expenses, supporting both small farms and larger agricultural operations.

With numerous loan options available, one of the most trusted and popular choices for small businesses is the SBA loan, which offers flexible terms and government-backed support.

SBA Loans (High Authority & Popular)

SBA loans are among the most popular funding options. The government supports them and provides small businesses with access to affordable financing, offering flexible repayment terms.

20. What is an SBA loan, and how does it work?

An SBA loan is partially guaranteed by the Small Business Administration, reducing lender risk. Businesses apply through banks or approved lenders, and the SBA backs a portion of the loan. This allows longer repayment terms, competitive rates, and better access to funding for small businesses.

21. What are the benefits of an SBA loan compared to traditional loans?

SBA loans often offer lower down payments, longer repayment terms, and more flexible credit requirements than traditional loans. They’re designed to support small businesses that might not qualify otherwise. Borrowers also benefit from competitive interest rates and access to higher loan amounts for growth.

22. Who offers SBA loans?

SBA loans are issued by approved lenders, including banks, credit unions, and some online lenders. The SBA doesn’t lend directly; it guarantees a portion of the loan, which encourages lenders to provide financing with more favorable terms to small businesses that might not meet standard requirements.

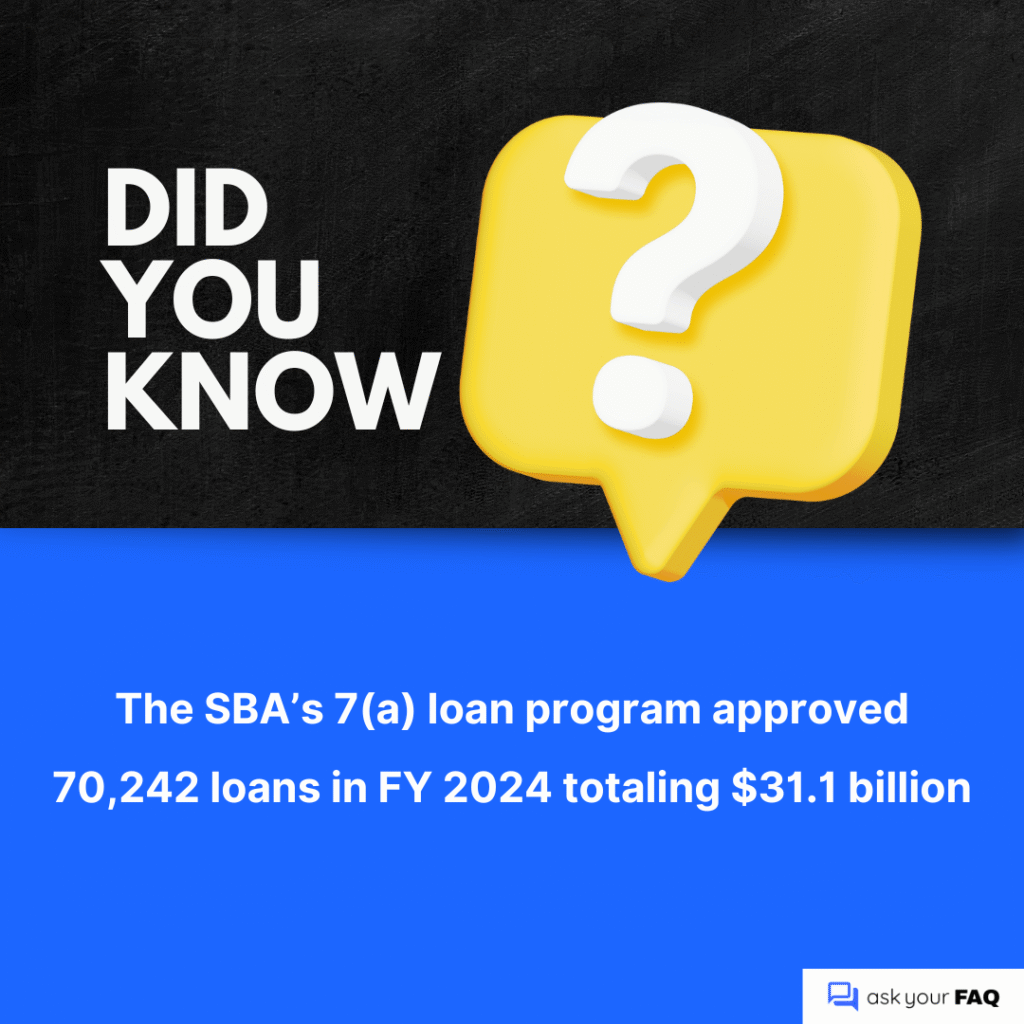

23. What are SBA 7(a) loans and SBA 504 loans?

SBA 7(a) loans are the most common, used for working capital or equipment. SBA 504 loans focus on long-term financing for fixed assets, including buildings and machinery. Both offer low rates and extended terms, but serve different needs depending on business goals.

24. Can SBA loans be used by startups, restaurants, or for commercial real estate?

Yes. SBA loans can fund a variety of businesses, including startups and restaurants. They’re also widely used for commercial real estate purchases, expansions, or refinancing. Eligibility depends on the business’s financials, management experience, and ability to repay; however, SBA programs cover a diverse range of industries and purposes.

25. What are the borrowing limits on SBA loans?

Borrowing limits vary depending on the SBA loan program. Some are designed for larger projects, such as real estate or equipment, while others are better suited for smaller funding needs. The right option depends on your business size, purpose, and overall financing requirements.

26. Are there SBA loan programs specifically for veterans?

Yes. The SBA offers programs like the Veterans Advantage, which reduces fees on particular 7(a) loans for veteran-owned businesses. Other organizations and state programs also provide discounted rates or flexible terms to support veterans transitioning into business ownership and expanding existing operations.

27. How long does SBA loan approval and funding usually take?

Approval times vary. Standard SBA loans may take several weeks due to document reviews and SBA involvement. However, SBA Express loans are faster, often providing approval within 36 hours and funding in a matter of days. Timing depends on the lender, loan type, and the completeness of the application.

28. Where can I find an SBA loan checklist to prepare my application?

The SBA website provides detailed loan application checklists. Many lenders also publish their own guides covering financial statements, tax returns, legal documents, and business plans. Using a checklist helps ensure all paperwork is ready, reducing delays and improving your chances of quick approval.

While SBA loans offer many advantages, it’s equally important to understand their interest rates and repayment terms so you can plan and manage your financing with confidence.

Interest Rates & Repayment

Knowing how interest rates are determined and how repayments work helps you pick the right loan, manage costs, and avoid surprises.

29. What factors determine the interest rate on a small business loan?

Interest rates depend on your credit score, business revenue, loan type, collateral, and the lender’s policies. SBA-backed loans typically offer lower rates, while unsecured loans or those with weaker credit may result in higher rates. Market conditions and repayment terms also influence the final rate offered.

30. Should I choose a fixed or variable interest rate?

Fixed rates remain constant throughout the life of the loan, providing predictable payments. Variable rates fluctuate in response to market changes, which can lower costs when rates drop but raise them if rates rise. Fixed rates suit stability-focused businesses, while variable rates are more suitable for those who are comfortable with some risk.

31. How are repayments structured for small business loans?

Repayments are typically monthly, covering both principal and interest. Some lenders offer weekly or biweekly options, especially for short-term or online loans. The structure depends on the loan type; term loans have set payments, while lines of credit require payments only on the amount drawn.

32. Can I pay off my small business loan early without penalties?

It depends on the lender. Many loans allow for early repayment without fees, resulting in savings on interest. However, some agreements include prepayment penalties or require interest guarantees. Always review loan terms carefully to understand whether paying early will incur additional costs or help you save money.

33. How can I lower my monthly loan payments?

Options include refinancing to a longer repayment term, consolidating multiple debts into one loan, or negotiating with your lender for adjustments. Improving your credit before refinancing may also help you secure better rates. Lower payments often mean paying more interest over time, so weigh short-term relief against long-term cost.

34. Do I pay interest if my line of credit balance is zero?

No. With a business line of credit, you only pay interest on the funds you actually use. If your balance is zero, there’s no interest charged. Some lenders may apply minor maintenance or annual fees, but you won’t accrue interest without drawing funds.

Understanding interest rates and repayment terms helps establish a solid foundation. The next step is to explore business lines of credit, a flexible funding option that differs from traditional loans.

Lines of Credit

A business line of credit offers flexible funds. Knowing how it works, its limits, and best uses helps manage cash flow.

35. What is the difference between a business line of credit and a business credit card?

| Feature | Business Line of Credit | Business Credit Card |

| Access to Funds | Flexible cash withdrawals as needed | Revolving credit for everyday purchases |

| Interest Rates | Typically lower | Often higher |

| Best For | Larger expenses, managing cash flow | Small, frequent, or everyday business expenses |

| Repayment | Based on the amount drawn | Monthly balance repayment, minimum due option |

36. How does the lender determine my credit line?

Lenders consider factors such as your revenue, cash flow, credit history, and the duration of your business. They may also weigh industry risk to decide on an amount that’s manageable for both sides.

37. What’s the process for moving from a secured to an unsecured line of credit?

Typically, businesses start with a secured line backed by cash or assets. After demonstrating consistent payments and financial stability, you can request an upgrade to unsecured status. The lender reviews your credit, revenue, and repayment history before removing the collateral requirement and extending more flexible terms.

38. What’s the minimum and maximum amount I can access with a business line of credit?

The range varies by lender. Stronger financials generally lead to higher limits, while smaller or newer businesses may qualify for more modest amounts.

While lines of credit offer flexibility, some businesses need financing for specific assets. That’s where auto loans, equipment loans, and practice loans provide targeted solutions to support growth.

Auto, Equipment & Practice Loans

Some businesses need loans for specific purposes. Auto, equipment, and practice loans provide tailored funding options that help cover the costs of vehicles, tools, or professional practice needs, offering flexible repayment terms.

39. What are small business auto loans, and how do they work?

Small business auto loans finance vehicles used for work, like trucks, vans, or service cars. The vehicle usually serves as collateral, which helps secure better rates. Loan terms depend on credit, business revenue, and vehicle type. These loans spread payments over time, making business vehicle purchases more affordable.

40. Can I refinance my existing small business auto loan?

Yes. Refinancing allows you to replace your current loan with a new one, ideally with a lower interest rate or a longer term. This can reduce monthly payments or save on interest. Approval depends on your current loan balance, credit, and business financials. Not all lenders offer refinancing options.

41. What loan options are available for equipment purchases or leasing?

Businesses can choose equipment loans or equipment leasing. Loans allow you to buy and own equipment, using it as collateral. Leasing provides use without ownership, often with lower monthly costs. Both options help manage upfront expenses, with the choice depending on cash flow and long-term business needs.

42. Do healthcare, dental, or veterinary practices qualify for specialized small business loans?

Yes. Many lenders and SBA programs offer tailored loans for medical, dental, or veterinary practices. Funds can be used for equipment, office setup, expansions, or working capital. These loans often have flexible terms, recognizing the stability and long-term revenue potential of healthcare-related businesses.

43. Are there practice loans available to doctors still in residency?

Some lenders and programs allow doctors in residency to apply for practice loans. Approval often depends on future earning potential, personal credit, and sometimes a cosigner. Loan amounts may be limited until full licensing, but options exist to help residents prepare for starting or buying a practice.

After securing the correct type of loan, the focus shifts to managing it effectively. Knowing how to handle payments, changes, and loan responsibilities will contribute to your long-term success.

Managing Loans (After Approval)

Getting approved is only the beginning. Managing your loan wisely, handling payments effectively, making necessary adjustments, and understanding your options helps keep your business finances healthy and stress-free.

44. Can I change the due date for my business loan payment?

Some lenders allow adjustments to payment dates, but policies vary. You’ll need to contact your lender directly to request a change. Approval often depends on your payment history and account standing. Changing dates may help with cash flow, but it’s not always guaranteed.

45. What happens if I sell my business? Can the loan be transferred?

Most business loans can’t be automatically transferred. The new owner usually must apply and qualify with the lender. In some cases, the buyer may assume the debt if approved. Otherwise, the loan balance must be repaid before or during the business sale process, unless the business files for bankruptcy, which may change how the debt is handled.

46. How do I request a statement showing interest paid for tax purposes?

You can typically request an interest statement through your lender’s online portal, by phone, or in person at a branch. Many lenders automatically issue annual statements at tax time. Keeping this record helps when filing deductions for business loan interest expenses with your accountant.

47. Who do I contact if I have questions about my business loan or line of credit?

The first point of contact is your lender’s customer service team or dedicated business banking representative. Larger loans may have assigned relationship managers. Always use official contact channels to discuss payments, balances, or terms of service. This ensures that you have accurate information and keeps your account secure.

Finding the Right Small Business Loan

Securing a small business loan means selecting a financing option that suits your specific needs. By understanding the eligibility requirements, necessary documents, and available loan options, you’ll know exactly what steps to take to secure the right loan for your business. The right loan helps manage cash flow, supports growth, and builds long-term stability, keeping your business financially strong and ready to seize opportunities.