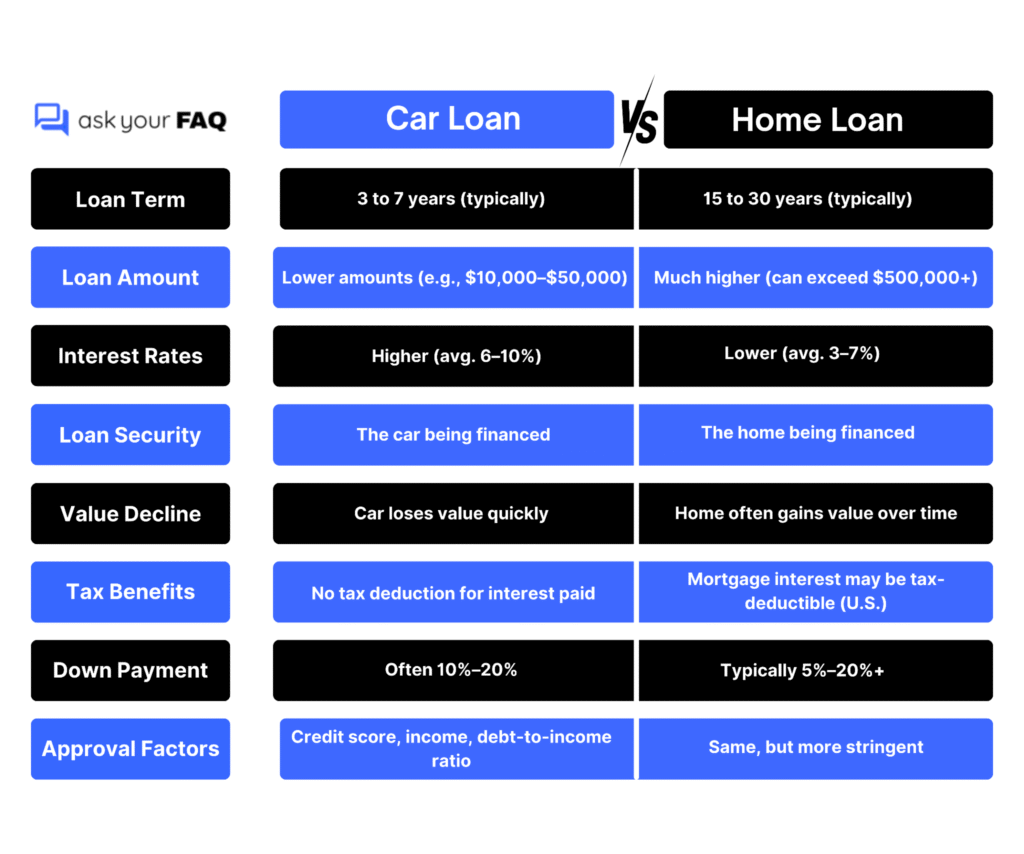

Car loans are one of the most common ways to finance a vehicle, with Americans taking out $187.9 billion in new auto loans in Q2 2025, according to the New York Fed. Understanding how these loans work is essential to avoid unnecessary costs. This blog explains how to apply for a loan, get approved with or without a strong credit history, and choose the right lender. With straightforward insights and real-world tips, you’ll be better prepared to make informed choices and manage your car loan more effectively.

How to Apply for a Car Loan

If you’re planning to finance your next vehicle, here’s how to apply for a car loan, get approved, and choose the best option based on your financial situation.

How can I get and apply for a car loan?

To get and apply for a car loan, follow these steps:

- Check your credit score to understand what loan terms you may qualify for.

- Decide on your budget and how much you can afford to borrow.

- Compare offers from banks, credit unions, and online lenders.

- Gather required documents such as proof of income, ID, and residence.

- Submit your application online or in person with details about your job, income, and the car you plan to buy.

- Review and accept the loan terms once approved. The lender will then send the funds directly to the dealer or seller.

How to Get Pre-Approved vs. Approved for a Car Loan

Getting pre-approved happens before you start shopping for a car. The lender reviews your finances and gives you a pre-approval letter stating how much you can borrow. This helps you set a budget, compare cars confidently, and negotiate better at the dealership.

Getting approved, on the other hand, happens after you’ve chosen your car and submitted a full loan application. The lender verifies your credit, income, and the vehicle details. Once approved, you’ll receive the final loan terms, including the amount, interest rate, and repayment period.

How much down payment is recommended?

A solid down payment helps you secure better loan terms, reduce monthly payments, and avoid owing more than the car is worth. While some lenders accept lower amounts, putting more down upfront can save you money on interest and make your loan more manageable.

How to get a car loan from a bank

To get a car loan from a bank, visit the bank’s website or branch to check its loan options. Apply by filling out the form and providing documents like income proof, ID, and credit details. The bank will review your credit history and income. If approved, they’ll offer a loan with terms like the interest rate and repayment period. Funds go directly to the dealer or seller.

How to get a car loan from a credit union

Credit unions often offer lower interest rates than banks. To get a car loan, you’ll usually need to become a member first. Then apply online or in person by providing your income, ID, and credit details. If approved, you’ll get a loan offer with repayment terms. Many credit unions also pre-approve members, helping you shop confidently within your loan limit.

How to get a loan for a used car

To get a loan for a used car, check your credit score and budget first. Then shop for lenders that finance used vehicles, including banks, credit unions, and online lenders. Make sure the car meets the lender’s requirements (such as age and mileage limits). Submit your loan application with documents like income and ID proof. Once approved, you’ll receive the funds to buy the used car.

Car Loans with Bad or Limited Credit

Even with limited or poor credit, you can qualify for a car loan by choosing the right lender and preparing your application carefully.

How to get a car loan with bad credit

- Check your credit report and fix any errors.

- Find lenders that specialize in bad-credit auto loans.

- Make a larger down payment to reduce risk and interest rates.

- Add a co-signer with good credit to strengthen your application.

- Compare multiple offers before choosing.

- Select lenders reporting to credit bureaus to rebuild your credit over time.

How to get a car loan with no credit

- Apply with a co-signer who has a good credit history to boost approval chances.

- Make a larger down payment to reduce lender risk and show financial commitment.

- Look for first-time buyer programs from lenders who work with new borrowers.

- Try credit unions or online lenders that are more flexible with credit requirements.

- Borrow a smaller amount and make timely payments to start building credit.

Can I get a car loan with a 500 credit score?

Yes, you can get a car loan with a 500 credit score, but it may come with a high interest rate and stricter terms. You’ll likely need to show proof of steady income and may be required to make a larger down payment. Consider applying through lenders who specialize in subprime auto loans. A co-signer or trade-in vehicle can also help improve your approval chances.

What is a good credit score for a car loan?

A good credit score for a car loan is typically 670 or higher. Scores above 720 often qualify for the best interest rates and loan terms. With a score in the 600s, you can still get approved, but you may pay more in interest. Lenders also consider your income, debt levels, and down payment when reviewing your loan application, not just your credit score.

Can you get a car loan without a job?

You can get a car loan without a job, but you must prove you have a steady income source, such as savings, retirement income, government assistance, or self-employment. Lenders want to see that you can make your monthly payments. A strong credit history, a co-signer, or a large down payment can also help increase your chances of getting approved without a traditional job.

Understanding Car Loan Interest Rates and APR

Knowing how interest rates and APR work can help you choose the right car loan and avoid paying more than you need to over time.

What is the average interest rate on a car loan?

As of 2025, the average interest rate for a 60-month car loan was 7.47% for new cars and 9.01% for used cars. While interest rates are typically lower for new vehicles, the monthly payments are often higher due to larger loan amounts. Rates can vary depending on credit score, lender, and loan terms.

What is the interest rate on a car loan?

The interest rate on a car loan is the cost you pay to borrow money from a lender. It’s expressed as a percentage of the loan amount and depends on factors like your credit score, loan term, and the lender’s policies. Interest is usually charged monthly and added to your payment, meaning the lower your rate, the less you’ll pay over time.

What is a good interest rate on a car loan?

A good interest rate depends on your credit score, but generally, anything below 5% for new cars and below 6% for used cars is considered good. Excellent credit borrowers may get rates under 4%, while average credit borrowers may see 6%–9%. To get the best rate, improve your credit, shorten the loan term, and compare offers from multiple lenders.

What is a good APR for a car loan?

A good APR for a car loan depends on your credit score. For borrowers with excellent credit, a good APR is typically around 5.18% or lower for new cars and 6.82% or lower for used cars. However, if you have poor credit, rates can rise significantly, sometimes over 15% for new cars and 21% for used cars. Always compare offers to find the most favorable terms.

How does APR work on a car loan?

APR stands for Annual Percentage Rate and represents the total yearly cost of your car loan, including interest and any fees. It helps you compare different loan offers more accurately than the interest rate alone. For example, a loan with a low interest rate but high fees may have a higher APR. The lower the APR, the less you’ll pay over the life of the loan.

How does interest work on a car loan?

Interest is the cost of borrowing money from a lender. With car loans, interest is usually simple interest, meaning it’s calculated on the loan’s remaining balance. Each monthly payment goes toward both interest and principal. Early in the loan, more of your payment goes to interest. As you pay down the principal, interest charges decrease, and more of your payment reduces the loan balance.

How to calculate interest on a car loan?

To calculate car loan interest, use this formula for simple interest:

Interest = (Loan Amount × Interest Rate × Loan Term in Years).

For example, if you borrow $20,000 at 5% interest for 5 years, the total interest is: $20,000 × 0.05 × 5 = $5,000.

This gives a rough estimate of total interest, not the monthly breakdown.

Refinancing and Managing Your Car Loan

If your current loan isn’t working for you, refinancing or making adjustments could lower your costs and give you more control over your payments.

How to refinance a car loan

To refinance a car loan, find a lender offering better rates or terms than your current loan. Apply with your financial details, including income and remaining loan balance. If approved, the new lender pays off your existing loan, and you start making payments under the new agreement. Refinancing can lower your monthly payment, reduce interest, or shorten the loan term, depending on your goal.

What happens if I miss a payment?

Missing a payment can trigger late fees and hurt your credit score. After 30 days, lenders typically report it to credit bureaus. Missed payments can lead to repossession, so contact your lender immediately if you’re struggling.

Can I refinance my car loan?

Yes, you can refinance your car loan if your credit score has improved, interest rates have dropped, or you want better loan terms. Most lenders allow refinancing as long as your vehicle holds enough value and your loan is in good standing. However, some fees or penalties may apply, so compare the total cost before deciding. Refinancing can save money or make payments more manageable.

How to get out of a car loan

To get out of a car loan, consider one of these options: sell the car and use the money to pay off the loan, refinance to lower your payments, or trade it in for a less expensive vehicle. If you owe more than the car’s value, you may need to pay the difference. Some people also voluntarily surrender the car, but this can hurt your credit.

How to get out of an upside down car loan

If you owe more on your car than it’s worth (called being “upside down”), options include: paying the difference when selling or trading the car, making extra payments to reduce the balance faster, or rolling the negative equity into a new loan (not ideal, as it adds debt). Refinancing might also help if you can get a lower interest rate to pay off the balance faster.

Can you transfer a car loan to someone else?

Most lenders don’t allow you to directly transfer a car loan to another person. However, the person can apply for a new loan to buy the car from you. If approved, their loan pays off your existing balance. This process effectively transfers the debt but requires lender approval and a full credit check on the new borrower.

How to transfer a car loan to a family member

To transfer a car loan to a family member, they’ll need to apply for a new loan in their name to pay off your existing one. If approved, your lender will be paid off, and the new loan will be under the family member’s name. You’ll also need to transfer the vehicle title. Always check with your lender first, as some do not allow this process

Can you remove a cosigner from a car loan?

Removing a cosigner usually requires refinancing the loan in your name only. Lenders typically won’t remove a cosigner without replacing the loan agreement. To refinance, you must qualify for the loan on your own based on income and credit. Once approved, the new loan replaces the old one, and the cosigner is no longer responsible for the debt.

Paying Off Your Car Loan Faster and Smarter

Paying off your car loan early can save money on interest. Here’s how to do it efficiently without affecting your budget or financial goals.

How to pay off a car loan faster

To pay off your car loan faster, make extra payments whenever possible, especially toward the principal. Choose a shorter loan term when refinancing or round up your monthly payments. You can also make bi-weekly payments instead of monthly. Check with your lender first to ensure there are no prepayment penalties or rules about how extra payments are applied.

Should I pay off my car loan early?

Paying off your car loan early can save money on interest and free up your monthly cash flow. It’s a good idea if you have no prepayment penalties and you don’t need the money for other high-interest debts. However, if your loan has a low interest rate and your money could earn more elsewhere (like investing or paying off credit cards), early payoff might not be necessary.

How to pay towards the principal on a car loan

To pay toward the principal, contact your lender or check your online loan portal. Make a separate payment or add an extra amount to your regular payment and label it as “principal only.” This reduces the balance faster and lowers the interest charged over time. Always confirm with your lender that the extra payment won’t be applied toward future interest or monthly payments.

What happens after I pay off my car loan?

After you pay off your car loan, the lender will send you a confirmation letter and release the lien on the vehicle. This means you fully own the car. You’ll receive a lien release document or a new title in your name, depending on your state. Make sure to store your payoff and title documents safely for registration or when selling the vehicle.

What is a maturity date on a car loan?

The maturity date is the final scheduled date when your car loan must be fully paid. It’s listed in your loan agreement. If you make all payments on time, this is when your last payment is due. Paying off the loan before this date is called early payoff. If you miss payments, the maturity date won’t change, but you may owe more due to late fees.

Selling or Trading In a Car That Has a Loan

Still owe money on your car? You can sell or trade it in, just be sure to understand how the loan payoff and title transfer work.

How to sell a car with a loan

To sell a car with a loan, first contact your lender to find out the payoff amount, what you owe in full. If you sell the car privately, the buyer pays you (or the lender), and you use that money to pay off the loan. If you owe more than the sale price, you’ll need to pay the difference. Once paid, the lender will release the title.

Should I trade in my car or sell it privately?

Selling privately usually nets you more money but takes more effort. Trading in is faster and more convenient, especially if you still owe on the loan. If you want the best value and can manage the sale, go private; otherwise, trade-in is simpler.

How to trade in a car with a loan

When trading in a car with a loan, the dealer will contact your lender to find the loan payoff amount. If the trade-in value is higher than what you owe, the extra goes toward your next car. If you owe more than the car’s value (negative equity), the dealer may roll the difference into your new loan, though this increases your new loan balance and interest cost.

Using Alternative Loan Options for Your Car

Not all car financing has to come from a traditional auto loan; explore other ways to borrow using personal loans, equity, or your vehicle itself.

Can I use a personal loan to buy a car?

Yes, you can use a personal loan to buy a car. Unlike auto loans, personal loans are unsecured, meaning they don’t use the car as collateral. You can buy from a private seller or a dealership. However, interest rates may be higher, especially if you have poor credit. It’s best for older or low-cost vehicles that may not qualify for traditional auto financing.

Can I use my car as collateral for a loan?

Yes, you can use your car as collateral to get a secured loan. This type of loan is called a title loan or an auto equity loan. The lender places a lien on your car title until the loan is paid. These loans often have higher interest rates and shorter terms. If you don’t repay, the lender can repossess your car, so use them carefully.

Where can I get a loan using my car as collateral?

You can get a loan using your car as collateral from banks, credit unions, online lenders, or title loan companies. Some lenders offer “auto equity loans” if you own your car or have significant equity in it. Always compare terms and interest rates carefully. Be cautious with title loan companies, as they often charge high fees and interest, increasing the risk of losing your vehicle.

Can you get a title loan on a financed car?

Getting a title loan on a financed car is difficult because the lender still holds the title. However, some lenders offer second-position loans based on the equity you’ve built. This means you owe less than the car is worth. These loans are riskier and usually come with high interest. It’s important to know that if you default, you could still lose your car to repossession.

Can you pay a car loan with a credit card?

Most lenders don’t accept direct credit card payments for car loans. However, you can sometimes use a credit card to make a payment indirectly through third-party services, but they often charge fees. Using a credit card may also add interest if you don’t pay it off quickly. Unless it’s a 0% interest card, it’s usually not a good idea to pay loans this way.

What is gap insurance on a car loan?

GAP insurance (Guaranteed Asset Protection) covers the difference between what you owe on your car loan and what your car is worth if it’s totaled or stolen. Regular auto insurance only pays the current market value, which may be less than your loan balance. GAP insurance protects you from having to pay that difference out of pocket, especially useful if you made a small down payment or have a long loan term.

Wrapping Up, Smarter Car Loan Decisions Start Here

Understanding how car loans work, from application and approval to refinancing and early payoff, can help you save money and avoid costly mistakes. Whether you have excellent credit or are working to improve it, knowing your financing options gives you greater control.

Always compare interest rates, review loan terms carefully, and choose what aligns with your financial goals. With the right knowledge, you can manage your car loan confidently and make smarter decisions throughout your vehicle ownership journey.