Running a business comes with a lot to handle. Between serving customers, paying bills, and keeping business moving, insurance often gets pushed aside. The problem is, many owners only think about it after something bad happens.

That’s why commercial insurance matters; it helps you stay open when accidents, lawsuits, or losses come your way. From basic coverage, such as general liability, to additional protection, like cyber insurance, each type plays a crucial role in keeping your business safe.

This blog will guide you through the most common insurance questions, enabling you to make informed choices and keep your business protected.

Getting Started with Business Insurance

Let’s start with the basics. If you’re new to business insurance, these questions will help you understand what it is, who needs it, and why it really matters.

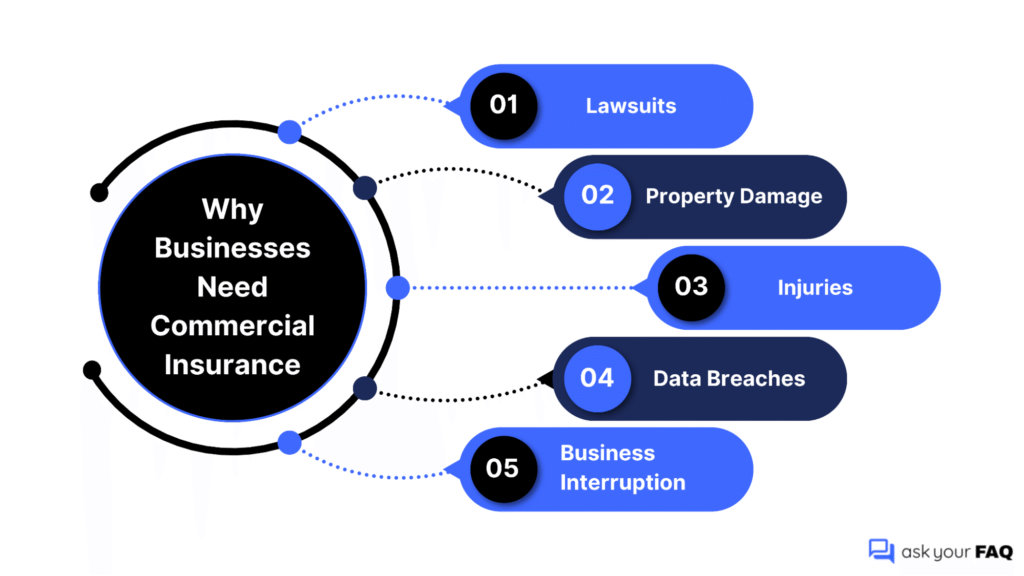

What is commercial insurance, and why do businesses need it?

Commercial insurance protects businesses from financial losses caused by accidents, lawsuits, theft, or property damage. It helps cover risks that could otherwise force your business to close, making insurance important for keeping your business safe, steady, and in many cases, legally required.

Here are the reasons businesses need commercial insurance.

What types of businesses need commercial insurance the most?

Any business that deals with customers, owns property, handles data, sells products, or employs staff should have commercial insurance. This includes contractors, retailers, consultants, freelancers, and service providers who face everyday risks that could lead to costly claims or damages.

How is commercial insurance different from personal insurance?

Personal insurance covers your individual life, health, home, or car. Commercial insurance protects a business’s operations, assets, employees, and legal liabilities. It addresses risks specific to running a business, like customer injuries, employee claims, or damage to business property and equipment.

Can I customize my commercial insurance coverage?

Yes. Most insurers let you mix and match policies to fit your specific needs. For example, a consultant might combine General and Professional Liability, while a retailer adds Property and Cyber coverage. Customizing prevents paying for coverage you don’t need.

Does commercial insurance protect against lawsuits?

Yes. Many commercial insurance policies cover legal costs if your business is sued. For example, General Liability Insurance helps with customer injury or property damage claims, while Professional Liability Insurance covers mistakes or bad advice. Without coverage, legal fees alone could quickly overwhelm a small business.

Does my home-based business need commercial insurance?

Yes. Homeowners insurance usually excludes business activities. If you run a home-based business, you may need coverage for work equipment, customer visits, or liability. Without it, losses from theft, fire, or accidents involving your business may not be covered at all.

Can freelancers and sole proprietors buy commercial insurance?

Absolutely. Freelancers and sole proprietors can get coverage tailored to their work. Common choices include professional liability insurance to handle client disputes, cyber insurance for data protection, or general liability for basic coverage. It protects their income and professional reputation from risks.

What type(s) of Business Insurance do I need?

Most businesses start with general liability for basic protection. Depending on your risks, you may also need professional liability, commercial property, cyber insurance, or a Business Owner’s Policy. The right mix depends on your industry, size, operations, and client requirements.

How do I know which commercial insurance policy is right for me?

The best approach is to identify your risks first. Then, compare policy options or work with an insurance broker. They’ll help match coverage to your industry, budget, and requirements, ensuring you don’t pay for protection you don’t need or miss coverage gaps.

Can one policy cover all my business needs, or do I need multiple policies to meet my requirements?

A Business Owner’s Policy combines several protections, but it rarely covers everything. You may need separate policies like workers’ compensation, commercial auto, or cyber coverage, depending on your business setup. Multiple policies ensure you’re fully protected across different areas of risk.

So now you know who needs commercial insurance and why. But what exactly does it cover? Let’s examine the primary types of policies and how each one safeguards your business.

Types of Coverage & What They Include

So, what does business insurance actually cover? Let’s walk through the main types of policies and how each one helps protect different parts of your business.

What is General Liability Insurance, and what does it cover?

General Liability Insurance protects against common business risks like customer injuries, property damage, and advertising mistakes. It’s often the first policy small businesses buy because it covers lawsuits and settlements that could otherwise create major financial problems.

What is Professional Liability Insurance, and who needs it?

Professional Liability Insurance, also known as Errors & Omissions, covers claims of negligence, mistakes, or poor advice that result in financial losses for a client. It’s essential for professionals like consultants, accountants, designers, and IT providers whose work directly affects clients’ results.

What is a Business Owner’s Policy (BOP) and what is included in it?

A Business Owner’s Policy combines General Liability and Commercial Property Insurance into a single package. Many also include business interruption coverage. BOPs simplify protection and often cost less than buying each policy separately, making them ideal for small businesses.

What is Workers’ Compensation Insurance, and when is it required?

Workers’ compensation covers medical bills, lost wages, and rehabilitation if an employee is injured or becomes ill while on the job. In most states, it’s legally required as soon as you hire your first employee, even part-time staff.

How does Commercial Auto Insurance work?

Commercial Auto Insurance covers vehicles used for business, such as delivery vans, trucks, or company cars. It covers accidents, injuries, and damages that occur while driving for work. Personal auto policies don’t cover vehicles when used for business purposes.

What is Commercial Property Insurance, and what does it protect?

Commercial Property Insurance is coverage that protects the physical assets of your business. This includes your building, equipment, tools, and inventory. It helps pay for repairs or replacement if they’re damaged by fire, theft, vandalism, or storms, whether you own or lease your workspace.

Is Cyber Liability Insurance necessary for small businesses?

Yes. Small businesses are frequent targets of cyberattacks. Cyber Liability Insurance helps cover costs from data breaches, ransomware, or stolen customer data. Without it, paying for legal fees, customer notifications, and recovery efforts could easily overwhelm a small business financially.

What is Umbrella Insurance for businesses?

Umbrella Insurance provides extra coverage once the limits of your existing liability policies are used up. It’s valuable protection for large claims or lawsuits, ensuring your business doesn’t face bankruptcy when damages exceed standard insurance policy limits.

If I have a home-based business, do I need property insurance?

Yes, you do. Standard homeowners insurance usually won’t cover business items or customer visits. If your laptop, tools, or stock are stolen or damaged, you’d pay out of pocket. Adding a commercial property policy or a rider gives real protection and keeps your business from unexpected losses.

Alright, now you’ve got a handle on what each policy actually does. But how much is this all going to cost, and what if you ever need to use it? Let’s get into that.

Costs, Payments & Claims

Insurance sounds great on paper, but what’s it going to cost, how do you pay for it, and what actually happens if something goes wrong? Let’s break it down.

Who decides the price of commercial insurance?

Insurance companies decide the price based on the risks your business faces. They consider factors such as your industry, location, claims history, number of employees, and coverage limits. Each insurer may calculate costs differently, which is why obtaining quotes from multiple providers is always a good idea.

What factors affect the cost of my business insurance premium?

Premiums depend on your industry, number of employees, revenue, location, and claims history. High-risk professions and businesses with a history of prior claims typically pay more. Coverage limits, deductibles, and optional add-ons also affect the price. Understanding these factors helps you budget and manage costs better.

Can I reduce my commercial insurance costs?

Yes. Bundle multiple policies with one insurer, raise your deductible, maintain safe business practices, and avoid unnecessary claims. Shopping around for quotes can also lower costs. Many insurers reward businesses with good safety records, which helps keep long-term premiums more affordable.

Do I have to pay the full amount upfront, or are there monthly options?

Most insurers offer monthly installments, making payments manageable for small businesses. However, you may save money by paying the annual premium upfront. Always confirm available payment options when choosing a provider, as terms can differ depending on the insurer and policy.

Can I get a discount by bundling policies together?

Yes. Insurers often give discounts when you combine multiple coverages, such as General Liability and Commercial Property, into a Business Owner’s Policy (BOP). Bundling not only saves money but also simplifies management, since you handle fewer separate policies and renewal dates.

What is a deductible, and how does it affect my premiums?

A deductible is the amount you must pay before insurance covers a claim. Higher deductibles lower premiums, but you’ll pay more upfront during claims. Lower deductibles cost more monthly but reduce out-of-pocket expenses later. Choosing depends on your cash flow and risk tolerance.

How do I file a claim for my business insurance?

Notify your insurer immediately after an incident. Provide details about what happened, share supporting documents like receipts or photos, and follow their instructions. Keep copies of everything submitted. Prompt, accurate reporting increases the chances of smooth processing and faster claim resolution.

How long does it take to process a commercial insurance claim?

Timeframes vary. Straightforward claims can be resolved within days, while complex cases may take weeks or longer. The speed depends on claim type, supporting documentation, and cooperation. Submitting complete information quickly and responding to insurer requests usually shortens the process significantly.

What if my claim is denied? Can I appeal it?

Yes. You can request a review or appeal, accompanied by additional evidence. Insurers sometimes deny claims due to missing information, exclusions, or misunderstandings. Carefully review the denial letter, clarify details with your insurer, and provide supporting documents to strengthen your case during appeal.

Does filing a claim increase my future premiums?

It can. Premiums may rise after a claim, especially if you file frequent or costly claims. Insurers view these as higher risk. One minor claim may not significantly impact costs, but a history of large claims can substantially increase costs at renewal.

So now you’ve got a grip on the money side, what it costs, how to pay, and what happens when stuff goes sideways. But what about the fine print, contracts, and real-world scenarios? Let’s get into that.

Practical and Legal Insights for Commercial Insurance

Insurance isn’t just about protection; it’s also about paperwork, contracts, and the rules you’ve got to follow. Here are the things business owners often overlook until they really matter.

Do I need proof of insurance to sign a commercial lease?

In most cases, yes. Landlords require proof of liability insurance before you can sign a commercial lease. This protects both parties in case accidents, damages, or lawsuits occur on the property. Without proof, many landlords won’t allow you to move in or operate legally within their space.

Will clients ask for a Certificate of Insurance (COI)?

Yes, many clients ask for a COI before signing contracts or starting work. A COI shows that your business is insured and reduces risk for them. It’s commonly requested in industries such as construction, consulting, and events, where liability concerns are high.

How often should I review or update my insurance policy?

You should review your insurance policy at least once a year or whenever your business changes. Adding employees, moving to a new location, or offering new services can create gaps in coverage, making it important to update policies to avoid potential uninsured risks.

What is a Waiver of Subrogation in commercial insurance?

A waiver of subrogation prevents your insurer from seeking reimbursement from another party after paying your claim. Often required in contracts, it protects business relationships by stopping lawsuits between partners, clients, or landlords, even if their negligence contributed to your financial loss.

Does my policy cover my employees or subcontractors?

Employees are usually covered under workers’ compensation and liability policies, but subcontractors often are not. Subcontractors typically need their own insurance unless added to your policy as additional insureds. Always confirm coverage with your insurer to avoid costly gaps in responsibility for accidents.

How do I add additional insured parties to my policy?

You can request additional insured parties by contacting your insurance provider. They’ll issue an updated policy endorsement and provide a Certificate of Insurance naming the party. This is commonly required in contracts with landlords, vendors, or clients and usually processed within a day.

What happens if I cancel my commercial insurance early?

If you cancel early, you may face a cancellation fee or lose prepaid premiums. Coverage ends immediately upon cancellation, leaving your business exposed to risks and possible contract breaches. Consider switching providers only after confirming continuous coverage to avoid being uninsured unexpectedly.

Can I buy short-term or temporary commercial insurance?

Yes. Short-term insurance is available for projects, events, or seasonal operations. It provides flexible coverage for limited periods when full annual policies aren’t needed. However, short-term policies may be more expensive per day and may not cover every risk, so it’s essential to check the details carefully.

Is business interruption coverage included in standard policies?

Business interruption coverage is not included in most basic policies. It’s typically part of a Business Owner’s Policy or added as an endorsement. It helps cover lost income and expenses if disasters, like fire, storms, or major damage halt your business operations.

How do I choose the right insurance provider for my business?

Choose a provider with experience in your industry, strong financial stability, and clear policy terms. Compare multiple quotes, review customer feedback, and check their claims process. The right insurer should offer tailored coverage, transparent pricing, and reliable support when you need it most.

What happens if I run my business without commercial insurance?

Operating without insurance means you cover all costs yourself if accidents, lawsuits, or damages occur. Even one claim could result in heavy legal fees, property replacement costs, or settlements, potentially forcing your business to close. Insurance helps manage these risks safely.

Commercial Insurance FAQ: Everything Business Owners Need to Know

Commercial insurance may feel confusing at first, but it’s really about one thing: protecting your business from risks you can’t always see coming. From simple liability coverage to specialized policies like cyber or property insurance, each type plays a role in keeping your work safe and your future steady.

The right coverage depends on your industry, size, and goals, but one thing is certain: not having protection can cost far more in the long run. Use this FAQ as a guide, ask questions, and choose policies that fit your needs. Your business deserves the peace of mind insurance brings.