Enrolling in Medicare for the first time can feel overwhelming. The rules are complex, the deadlines are strict, and one wrong decision can lead to lifelong penalties or unexpected healthcare costs. Many people are unsure when to enroll, what each part covers, or how to choose the right plan without overpaying.

This Medicare FAQ is designed to answer those questions clearly and directly. It breaks down how Medicare works, when you need to act, and what options matter most for first-time enrollees. Each question focuses on real concerns people face before turning 65, helping you make informed decisions without confusion or guesswork.

Medicare Basics

1. What is Medicare?

Medicare is a federal health insurance program mainly for people age 65 and older. It also covers certain younger individuals with disabilities or specific medical conditions. Medicare helps pay for hospital care, doctor visits, and prescription drugs.

2. Who is Medicare for?

- Individuals age 65 or older

- People under 65 with qualifying long-term disabilities

- Individuals diagnosed with specific conditions, such as End-Stage Renal Disease or ALS

- U.S. citizens or eligible permanent residents who meet residency requirements

3. Is Medicare free?

Medicare is not entirely free. Many people receive Part A without a premium, but Part B, Part D, and Medicare Advantage plans usually have monthly premiums, deductibles, and out-of-pocket costs.

4. What are the four parts of Medicare?

- Part A covers hospital care

- Part B covers medical services

- Part C, also called Medicare Advantage, combines Parts A and B through private insurers

- Part D covers prescription drugs

5. What is the difference between Original Medicare and Medicare Advantage?

Original Medicare includes Parts A and B and allows nationwide provider access. Medicare Advantage plans are offered by private insurers and often include additional benefits, but may require using provider networks.

Eligibility and Enrollment

6. When am I eligible to enroll in Medicare?

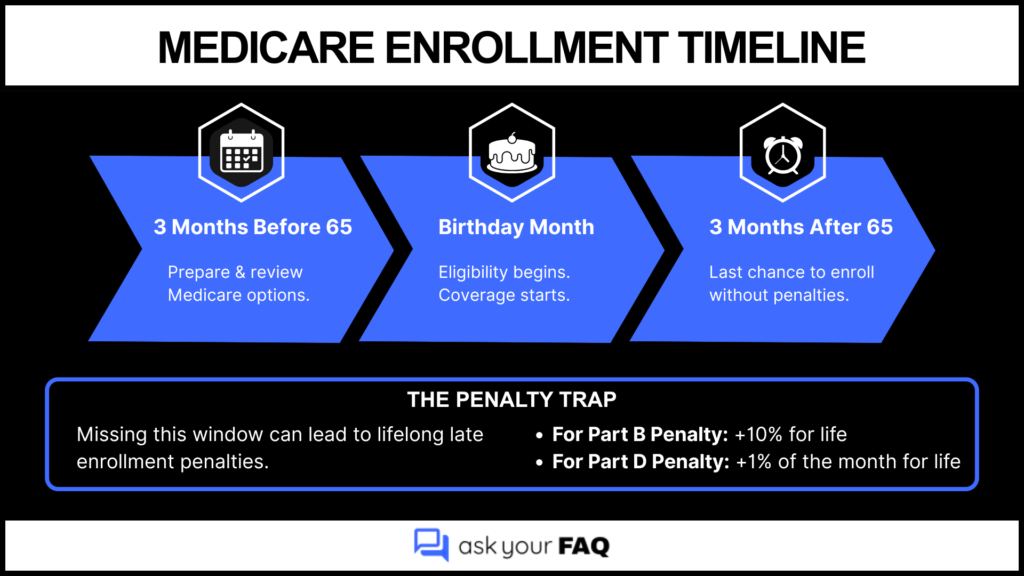

You are eligible to enroll during your Initial Enrollment Period, which is a seven-month window tied to your 65th birthday. It begins three months before your birthday month, continues through the month you turn 65, and ends three months after. Enrolling on time helps you avoid coverage delays and late enrollment penalties.

7. What happens if I miss my Medicare enrollment window?

If you miss your enrollment window, you may have to wait months for coverage to begin and pay late enrollment penalties. Part B and Part D penalties are added to your monthly premium and usually last for as long as you have Medicare, increasing your long-term healthcare costs.

8. Are you automatically enrolled in Medicare?

You are usually automatically enrolled in Medicare Part A and Part B if you are already receiving Social Security or Railroad Retirement Board benefits before turning 65. If you are not receiving these benefits, you must actively enroll in Medicare during your eligibility period to avoid delays or penalties.

9. Do Social Security benefits affect Medicare enrollment?

Yes. If you are already receiving Social Security benefits, you are typically enrolled in Medicare Part A and Part B automatically. If you delay Social Security, Medicare does not start on its own, and you must enroll manually during your eligibility period to avoid penalties or coverage gaps.

10. What are the Medicare enrollment periods?

- Initial Enrollment Period

- General Enrollment Period from January 1 to March 31

- Annual Enrollment Period from October 15 to December 7

- Special Enrollment Periods due to qualifying life events

Signing Up for Medicare

11. How do I sign up for Medicare?

You can sign up for Medicare through the Social Security Administration in several ways. Most people enroll online, which is the fastest and most convenient option. You can also enroll by phone or by visiting a local Social Security office if you prefer in-person assistance.

12. Is enrolling in Medicare the same as choosing a Medicare plan?

No. Enrolling in Medicare gives you access to Part A and Part B through the federal program. Selecting additional coverage such as Medicare Advantage, Part D prescription drug plans, or Medigap insurance is a separate decision made through private insurance companies.

13. Can I enroll in Medicare online?

Yes. You can enroll in Medicare online through the Social Security Administration website. This option allows you to complete your application at your own pace without visiting an office, and it is the most commonly used method for first-time enrollees.

14. How do I enroll in Medicare Advantage or Part D plans?

You enroll in Medicare Advantage or Part D plans through private insurance companies approved by Medicare. Enrollment can be completed online, over the phone, or with help from a licensed insurance agent during an eligible enrollment period.

15. How does Medigap enrollment work?

Medigap plans are purchased from private insurers and are best enrolled during your Medigap Open Enrollment Period, which starts when you first enroll in Part B.

Understanding Coverage and Plans

16. What are the most common Medicare plans?

The most common Medicare options include Original Medicare, which consists of Part A and Part B, Medicare Advantage plans such as HMOs and PPOs offered by private insurers, standalone Part D prescription drug plans, and Medigap plans that help cover out-of-pocket costs under Original Medicare.

17. What is a Medicare HMO plan?

A Medicare HMO plan requires you to use doctors and hospitals within the plan’s network for most services. You typically need a primary care doctor and referrals to see specialists. These plans often have lower monthly premiums but less flexibility in choosing providers.

18. What is a Medicare PPO plan?

A Medicare PPO plan allows you to see both in-network and out-of-network providers without referrals. While staying in-network usually costs less, PPO plans offer more freedom to choose doctors and specialists, often at a higher monthly premium.

19. How do I choose the right Medicare plan?

Choosing the right plan depends on your healthcare needs and financial priorities. Consider your current health conditions, prescription medications, preferred doctors, travel frequency, and budget. The goal is to balance coverage, provider access, and predictable costs over time.

20. Can I change my Medicare plan later?

Yes. You can change Medicare Advantage or Part D plans during the Annual Enrollment Period each year. You may also qualify for a Special Enrollment Period if you experience certain life events, such as moving or losing other coverage.

Costs and Financial Considerations

21. What costs should I expect with Medicare?

Costs may include monthly premiums, deductibles, copayments, coinsurance, and prescription drug expenses. Costs vary depending on the plans you choose.

22. What are out-of-pocket costs?

Out-of-pocket costs include deductibles, copays, coinsurance, and services Medicare does not cover, such as certain dental or vision services.

23. How do I pay for Medicare?

- Monthly premiums are usually deducted from your Social Security benefits

- If you are not receiving Social Security, Medicare sends a quarterly bill

- You can pay bills by mail, online banking, or Medicare Easy Pay

- Some plans may bill premiums directly through private insurers

24. Are there programs to lower Medicare costs?

Yes. Several assistance programs are available for people with limited income or resources. Programs such as Extra Help can reduce prescription drug premiums and copays, while state Medicare Savings Programs may assist with Part A and Part B premiums, deductibles, and coinsurance costs.

25. Should I enroll in Part D even if I take no medications?

Yes. Enrolling in Part D when you are first eligible helps you avoid late enrollment penalties that increase your premium permanently. Having coverage in place also protects you financially if your medication needs change unexpectedly in the future.

26. What is a Medicare formulary?

A formulary is the list of prescription drugs covered by a Medicare Part D or Medicare Advantage plan. Each plan maintains its own formulary and groups medications into pricing tiers, which affect how much you pay for each prescription.

Using Medicare

27. Can I use Medicare out of state?

Original Medicare generally allows you to receive care anywhere in the United States as long as the provider accepts Medicare. Medicare Advantage plans may limit routine care to their service area, but must cover emergency and urgent care nationwide.

28. How do claims work with Medicare?

Most doctors, hospitals, and pharmacies submit claims directly to Medicare on your behalf. If you use Original Medicare and a provider does not file a claim, you can submit one yourself for reimbursement using a Medicare claim form.

29. Does Medicare cover emergencies?

Yes. Medicare covers emergency medical care anywhere in the United States. Medicare Advantage plans are also required to cover emergency and urgent care services, even if you are outside the plan’s normal service area.

30. Does Medicare cover preventive care?

Yes. Medicare covers many preventive services, including annual wellness visits, screenings, vaccines, and counseling services. Many preventive services are covered at no cost when eligibility guidelines are met, and the provider accepts Medicare.

Ongoing Management and Support

31. How do I renew or update my Medicare coverage?

Medicare coverage renews automatically each year if you take no action. However, changes to Medicare Advantage, Part D, or supplemental plans must be made during designated enrollment periods if your healthcare needs or costs change.

32. What resources help explain Medicare terms?

Several trusted resources provide clear, unbiased Medicare information, including State Health Insurance Assistance Programs, the official Medicare website, and government-published Medicare guides designed for beneficiaries.

33. How do I contact Medicare?

You can contact Medicare by calling its official customer service number, visiting the Medicare website, or using local assistance programs for help with coverage questions and enrollment issues.

34. Who should seek help before enrolling?

First-time enrollees, individuals with ongoing medical conditions, and those comparing multiple plan options should seek guidance to avoid enrollment mistakes, penalties, or choosing coverage that does not meet their healthcare needs.

Related Reads

34 Homeowners Insurance FAQ: Answers on Cost & Coverage

Health Insurance FAQ: Clear Answers on Costs, Coverage, and Eligibility