A car accident can leave you with more than just physical injuries; it can trigger stress, confusion, and a flood of unanswered questions.

From understanding your rights to determining the amount of compensation you are entitled to, navigating the legal process can be complex and challenging. That’s why we’ve compiled this comprehensive FAQ on personal injury.

Here, you’ll find clear, direct answers to the most common concerns accident victims face, covering everything from injury recovery and case strength to insurance coverage, timelines, and legal fees.

Whether you’re still experiencing pain, struggling with medical bills, or considering a lawyer, this guide will help you take informed and confident steps forward.

Injury Severity & Recovery

The way your injuries affect your health and recovery plays a significant role in your claim. Understanding this connection helps you see how compensation is determined and what to expect.

How does injury severity affect my claim’s value?

The more severe your injury, the higher your potential compensation. Serious injuries often require extensive treatment, cause long-term pain, and impact earning ability, increasing damages for medical costs, lost wages, and suffering. Minor injuries usually result in lower settlements, but they still deserve a fair recovery.

Should I wait until I’ve recovered before settling?

Yes. Settling before you reach maximum medical improvement can undervalue your claim because you may not yet know the full extent of your injuries. Waiting allows all treatment costs, ongoing care needs, and potential long-term effects to be accurately calculated. Once you accept a settlement, you generally can’t reopen the case or seek additional compensation later.

Can I claim compensation for emotional trauma or PTSD?

Yes. Emotional trauma, anxiety, and PTSD are recognized damages in personal injury cases. You’ll need documentation from mental health professionals to support your claim, and it may significantly increase compensation, especially when psychological effects affect daily life and relationships.

Do I need to complete all my medical treatment before filing a claim?

No, you don’t need to finish treatment before filing. In fact, starting the claim early helps preserve evidence and ensures compliance with deadlines. However, it’s best to wait until you have reached maximum medical improvement before settling, so that future treatment costs are fully included.

Will ongoing treatment affect when I can settle?

Yes. If your medical treatment is ongoing, it’s generally best to wait before settling so all future care costs can be factored into your claim. Settling too early could leave you responsible for significant future bills out of pocket, reducing your overall recovery. Taking the time to fully assess your needs often leads to a fairer and more accurate settlement.

Your injuries set the foundation for your claim. Next, it’s essential to understand what makes a case strong and the legal challenges that could affect your results.

Case Strength & Legal Challenges

Many accident victims worry whether their case is strong enough to win. Knowing the key factors that strengthen your claim and the challenges that can weaken it helps you stay prepared and avoid costly mistakes.

How do I find a personal injury lawyer specializing in car accidents?

Look for lawyers specializing in personal injury who have strong reviews, proven case results, and offer free consultations. Ask about their experience with similar accidents, trial readiness, resources for handling complex claims, and success rates.

Recommendations from friends, online legal directories, or local bar associations can also point you toward trusted professionals who understand your state’s specific laws.

Is it worthwhile to hire a personal injury lawyer?

Yes. A skilled lawyer can maximize compensation, handle insurance negotiations, gather evidence, and manage deadlines. Without one, you risk undervaluing your claim or missing legal requirements. Studies show that represented victims typically recover significantly more than those handling cases alone.

What evidence will make my case stronger?

To build a compelling claim, gather as much clear documentation as possible. The following types of evidence can significantly strengthen your case:

- Accident reports – official police or incident reports detailing the crash.

- Medical records – diagnoses, treatments, and bills proving injury and care.

- Witness statements – testimonies from people who saw the accident.

- Photographs & videos – of the accident scene, vehicle damage, and injuries.

- Proof of lost income – pay stubs, employer letters, or tax records.

- Documentation of pain & emotional distress – journals, therapy notes, or evaluations.

- Impact on daily life – evidence showing reduced quality of life or ability to work.

Collecting these documents not only supports your claim but also helps your attorney present a clear and persuasive case on your behalf.

Can I still win my case if I was partially at fault?

Yes, that’s how comparative negligence works. You’re still eligible for compensation even if you share some blame, but the amount is reduced based on your percentage of fault.

This ensures a fairer outcome, especially in cases where fault isn’t clear-cut. Just note that some states have modified comparative negligence rules, which may bar recovery if your share of fault crosses their legal threshold.

What legal challenges could weaken my claim?

Having an experienced attorney can help counter these challenges and ensure the full value of your claim is protected.

- Missed filing deadlines – waiting too long can bar your claim altogether.

- Inconsistent statements – differing accounts can damage credibility.

- Lack of evidence – weak documentation makes it harder to prove liability.

- Disputed injury cause – insurers may argue injuries weren’t accident-related.

- Pre-existing conditions – used to minimize or deny your compensation.

- Partial fault arguments – insurers may claim you share responsibility.

- Insurance company tactics – delay, lowball offers, or misrepresentation.

Being aware of these potential challenges early on allows you and your attorney to address them proactively, strengthening your case and improving your chances of fair compensation.

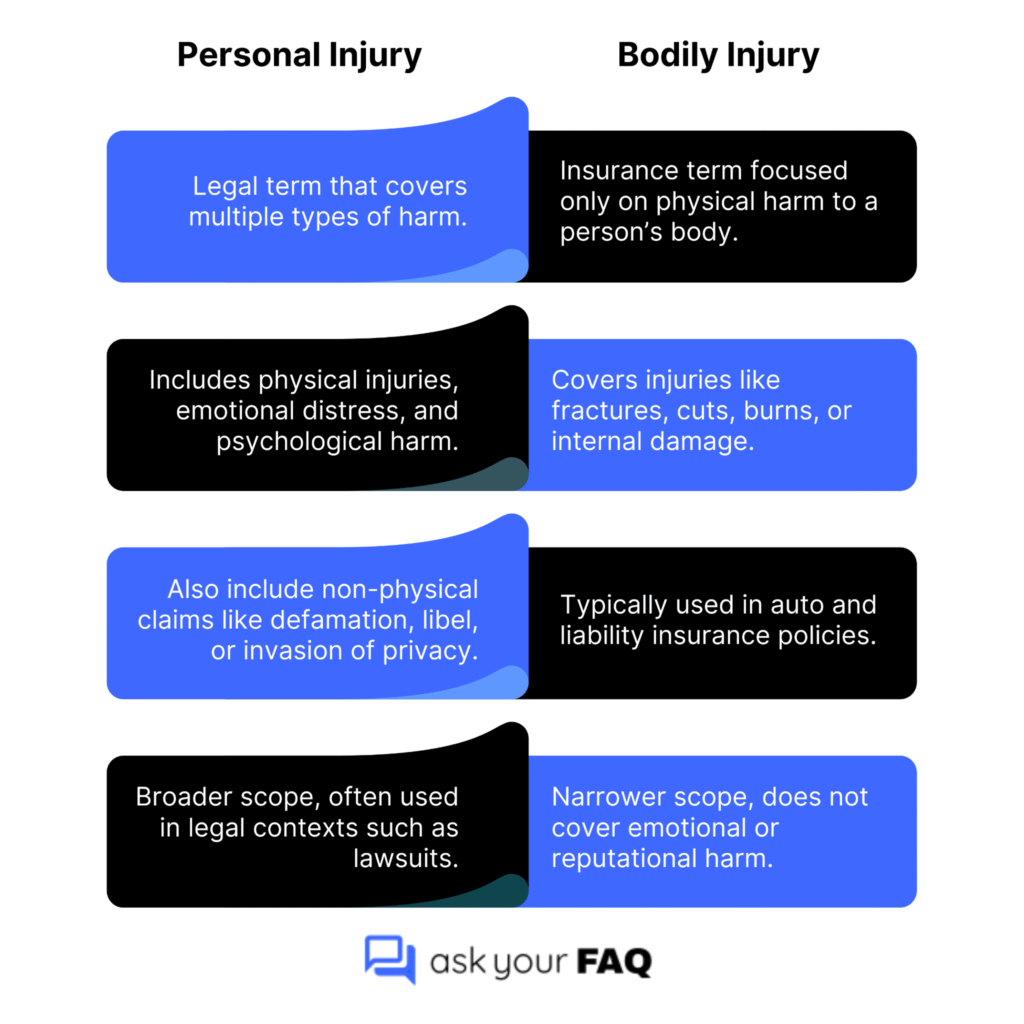

What’s the difference between personal injury and bodily injury?

Bodily injury refers only to physical harm, often in insurance policies. Personal injury is broader, encompassing physical, emotional, mental, and financial damages. A personal injury claim can cover pain and suffering, lost wages, medical costs, and other related expenses.

Settlement Value & Compensation

Knowing what strengthens your case and what weakens it is only half the battle. The next step is understanding settlement value, how compensation is calculated, and what damages you can claim.

How is the settlement value for my case calculated?

Several key factors go into determining the settlement value of a case. These typically include:

- Medical costs – hospital bills, treatment, rehabilitation, and prescriptions.

- Lost wages – income lost during recovery and potential future earnings.

- Future treatment needs – surgeries, therapy, or long-term medical care.

- Pain and suffering – physical pain, emotional distress, and reduced quality of life.

- Impact on daily life – limitations in work, hobbies, or family responsibilities.

- Severity of injury – more serious injuries typically result in higher compensation.

- Fault percentage – your share of responsibility may reduce settlement value.

- Insurance limits – coverage caps often restrict the maximum amount that can be paid out.

Because every case is unique, these factors are weighed differently depending on your circumstances. Working with an experienced attorney can help ensure all relevant damages are considered and that you pursue the maximum compensation available.

What types of damages can I claim (medical, lost wages, pain & suffering)?

The damages you can claim will generally include:

- Economic damages – medical bills, rehabilitation costs, lost wages, and reduced earning capacity.

- Non-economic damages – pain and suffering, emotional distress, and loss of enjoyment of life.

- Punitive damages – in rare cases, awarded to punish especially reckless or negligent behavior.

An attorney can help determine which damages apply to your case and ensure they are fully pursued.

Can I get compensation for future medical expenses?

Yes, if your injuries require ongoing or future treatment. This includes surgeries, therapy, medications, and long-term care. Medical experts often provide cost projections, which your lawyer will use to ensure your settlement covers not just current bills, but future needs too.

How do I know if the insurance company’s offer is fair?

Compare the offer to your documented losses, future costs, and the value of your legal case. If it’s much lower, it’s likely a lowball attempt. A personal injury lawyer can assess fairness, negotiate better terms, and ensure you’re not pressured into settling too soon.

Now that you know how settlements work, the next step is to understand insurance coverage and limits, since they play a significant role in what you can actually receive.

Insurance Coverage & Limits

One of the biggest worries after an accident is who will actually pay for the damages. Understanding how insurance coverage and policy limits work helps you know what compensation is truly available.

How do insurance policy limits affect my payout?

Exactly. Insurance companies will only pay up to the at-fault driver’s policy limits. If your damages go beyond that:

- Underinsured motorist coverage (if you have it) can help cover the gap.

- Personal lawsuit against the at-fault driver is another option, but success depends on whether they have sufficient personal assets.

- Settlement negotiations may also consider policy limits as a ceiling, even if your losses are higher.

Understanding the at-fault party’s limits early helps your legal team plan the best route to full compensation.

What if the other driver doesn’t have insurance or is underinsured?

You can file a claim under your uninsured/underinsured motorist coverage if you have it. Without it, recovery may involve suing the driver directly, though collecting may be difficult if they lack assets. An attorney can explore other compensation sources, like third-party liability or employer responsibility, if the driver was working at the time of the accident.

Can I use my own insurance if the at-fault driver is unable to pay for the damages?

Yes. Your collision or uninsured/underinsured motorist coverage can help cover medical bills, vehicle repairs, and lost wages if the at-fault driver can’t pay. Using your own insurance may involve a deductible, but your insurer can often recover those costs later through subrogation, which is the process of seeking reimbursement from the responsible party or their insurer.

How do medical payment (MedPay) and PIP coverage work?

MedPay and PIP are two types of auto insurance coverage that help with medical costs after an accident, but they work differently. Here’s how they compare:

| Coverage Type | What It Covers | Fault Requirement | Extra Benefits | Availability |

| MedPay (Medical Payments) | Medical bills for you and passengers (doctor visits, hospital stays, ambulance costs) | Pays regardless of fault | Limited strictly to medical expenses | Available in many states, but optional |

| PIP (Personal Injury Protection) | Medical bills plus lost wages, rehab, and other related expenses | Pays regardless of fault | Broader protection, including non-medical costs | Required in “no-fault” states; optional elsewhere |

Understanding these differences helps you choose the right coverage based on your state’s requirements, your budget, and how much protection you want.

Will my premiums go up if I file a personal injury claim?

If you’re not at fault, many insurers won’t raise premiums. However, some do after any claim, depending on your state and policy. Using certain coverages, such as collision or PIP, may still impact rates. Your attorney or agent can clarify your insurer’s practices.

Understanding insurance and policy limits reveals the amount of money available. The next step is to understand the process, including how a personal injury case progresses and the typical timeframe for its resolution.

Case Process & Timeline

One of the most challenging aspects of the aftermath of an accident is uncertainty about the duration of the case. Learning the main steps and timeline helps you understand what to expect and plan accordingly.

How long will my personal injury lawsuit take?

Most cases settle within months, but complex or contested ones can take a year or more, especially if they go to trial. Timelines depend on factors such as injury recovery, evidence gathering, negotiations, and court scheduling. Delays are common, but patience often leads to stronger evidence and a better settlement outcome that fairly reflects long-term impacts.

What are the main steps in a personal injury case?

The main steps in a personal injury case usually include:

- Investigation – reviewing accident details and liability.

- Gathering evidence – collecting reports, medical records, witness statements, and photos.

- Filing the claim – notifying the insurance company and responsible parties.

- Negotiation – your lawyer works to reach a fair settlement with insurers.

- Filing a lawsuit – if the settlement fails, the case is taken to court.

- Trial – a judge or jury decides compensation if no agreement is reached.

Medical treatment and documentation continue throughout, supporting the value of your claim.

How soon should I file a claim after an accident?

File as soon as possible to meet your state’s statute of limitations, which is typically one to three years. Early filing also preserves evidence and the memories of witnesses. Even if recovery takes time, starting the process early strengthens your case and avoids missed deadlines.

What happens if my case goes to trial instead of settling?

If the settlement fails, both sides present evidence and witnesses in court. A judge or jury decides liability and damages. Trials take longer and carry some risk, but they can result in higher awards if your case is strong and well-prepared. Your attorney will guide you through the process, including pre-trial motions, jury selection, and courtroom strategy.

What happens if I miss the deadline to file my claim?

Missing the statute of limitations usually means losing your right to seek compensation, no matter how valid your case is. These legal deadlines vary by state and case type, sometimes as short as one year. Acting quickly is essential. A lawyer can help you determine the exact deadline, gather needed evidence, and file your claim before time runs out.

Now that you understand the process and timeline, the next thing to consider is the legal fees, how lawyers charge, and the costs you might incur.

Legal Fees & Payment

Many people worry they can’t afford a lawyer after an accident. Understanding how legal fees work will help you explore the available options and provide peace of mind regarding costs.

How do personal injury lawyers charge for their services?

Most personal injury lawyers work on a contingency fee basis. This means you don’t pay anything up front. Instead, they take 30-40% of your settlement or court award if you win. If you don’t win, you typically owe nothing. This setup aligns their motivation with yours; both of you benefit from a successful outcome. Always review the agreement carefully to understand the fee structure.

What is a contingency fee, and how does it work?

A contingency fee means your lawyer’s payment depends on winning your case. If you win, their fee is a set percentage of the compensation recovered. If you lose, you typically owe no attorney fees, though you may still cover certain case expenses like filing fees, expert witness costs, or administrative charges.

Are there upfront costs I need to pay?

Usually no. Most personal injury lawyers cover filing fees, expert witness costs, and investigation expenses upfront on your behalf. These costs are typically reimbursed from your settlement if you win, but it’s essential to clarify how they’re handled. Always review and confirm the terms in your retainer agreement carefully to avoid any unexpected deductions or financial surprises later on.

Will I owe anything if I lose my case?

With most contingency agreements, you won’t owe attorney fees if you lose. However, some contracts still require you to cover certain case-related expenses, such as court filing fees, expert witness reports, or administrative costs. Clarify these details with your lawyer before signing so you fully understand your potential financial responsibilities and overall risk.

Can legal fees be negotiated?

Exactly. Many lawyers are open to adjusting their contingency fee, especially if the case is straightforward or the expected settlement is high. It’s best to discuss this early, before signing anything. Always make sure the final agreement is in writing, clearly outlining what’s covered and any potential extra costs. This avoids confusion and ensures transparency from the start.

Personal Injury FAQ Key Takeaways

This personal injury FAQ provides clear answers to some of the most common questions people face after an accident, covering recovery, evidence, compensation, insurance, timelines, and legal fees. While the process can seem overwhelming, having the right lawyer helps protect your rights and ensures you get fair compensation.

Don’t feel pressured to accept a quick settlement or face insurance companies on your own. Instead, focus on your recovery and let the proper support guide you through the process. With patience and good legal help, you’ll be in a stronger position to move forward confidently.