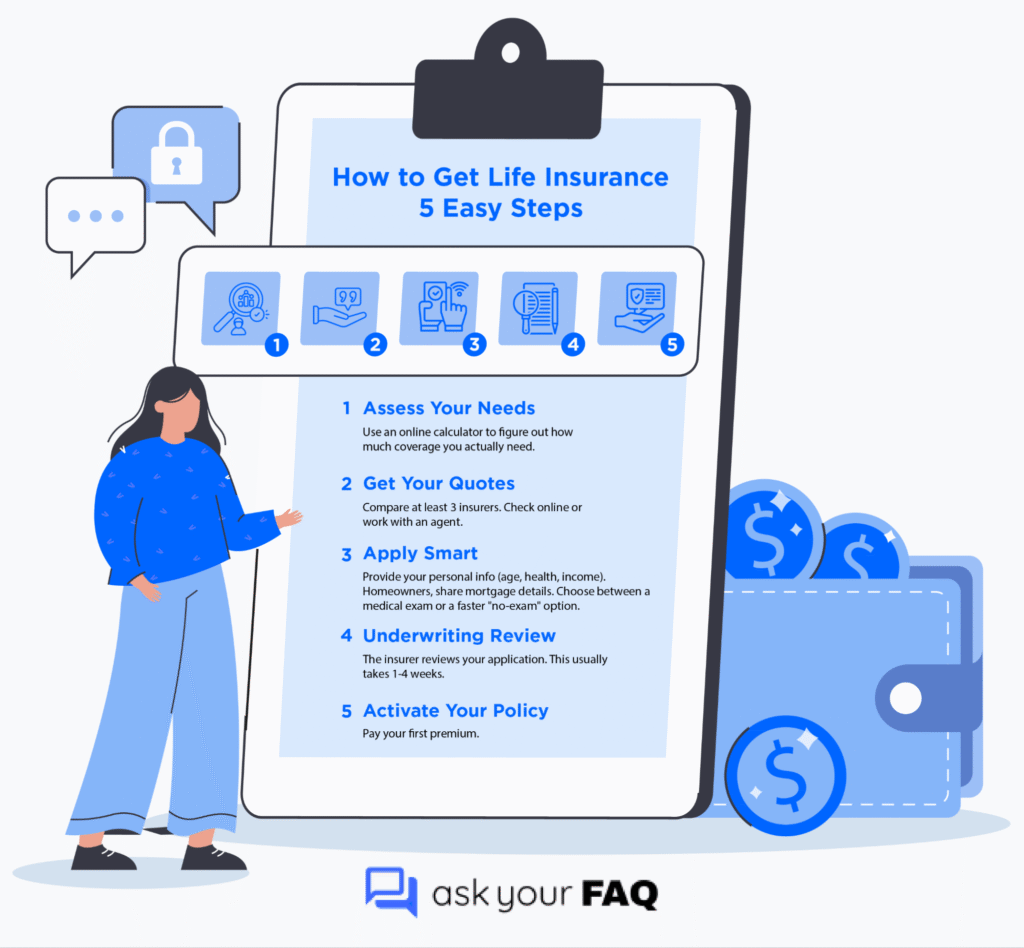

The world of life insurance can feel like a complex puzzle when you’re just starting. That big, confusing feeling often stops people from doing anything, which leaves a huge hole in their money plans.

We’re breaking down life insurance into clear, actionable steps, showing you exactly what to expect, what to look for, and how to get coverage that truly serves your first-time buyer needs.

Let’s simplify the process so that you can act with confidence.

Life Insurance FAQs Asked by First-Time Buyers

Entering the world of life insurance for the first time can bring up a lot of questions. To help you get started, here are some of the most common concerns and inquiries from first-time buyers like yourself:

- What’s the typical age range when people first consider life insurance?

While there’s no single “right” age, many people start considering life insurance in their late 20s to mid-30s, often coinciding with major life events like buying a first home, getting married, or starting a family.

- Is there a waiting period before my life insurance coverage actually begins?

Yes, there can be. After you apply, the insurer goes through an underwriting process. Coverage typically begins only after your application is approved, the first premium is paid, and the policy is “in force.”

- Can I get life insurance if I’m self-employed or have an irregular income?

Absolutely. Your income structure won’t prevent you from getting coverage. Insurers will typically look at your average income over a period (e.g., the last two years) to determine your insurable interest and the appropriate coverage amount.

- What’s the difference between group life insurance (from an employer) and individual life insurance?

Group life insurance, often provided by employers, is usually a basic amount of coverage that isn’t portable if you leave the job. Individual life insurance is purchased directly by you, is owned by you, and generally offers more comprehensive coverage that stays with you regardless of employment.

- How do I choose between getting a policy online versus through a traditional agent?

Online platforms often offer quicker, streamlined applications and potentially lower rates for straightforward term policies. A traditional or independent agent can provide personalized advice, help navigate complex situations, and compare multiple policies, which can be invaluable for custom needs.

- Can I convert a term life policy into a permanent life policy later on?

Many term policies offer a “convertibility” feature, allowing you to convert them into a permanent policy (like whole or universal life) without a new medical exam, typically before a certain age or within a specified timeframe.

- What happens to my term life policy when the term ends?

When the term ends, your coverage typically ceases unless you renew it (often at a significantly higher premium), convert it, or purchase a new policy.

- Are life insurance payouts taxable for my beneficiaries?

Generally, life insurance death benefits are paid out to beneficiaries income tax-free. However, there can be exceptions, such as if the policy is part of a taxable estate or certain complex trust arrangements.

- What is a “grace period” for premium payments?

A grace period is a specified length of time (usually 30 or 31 days) after your premium due date during which you can still make a payment without your policy lapsing. Your coverage remains active during this period.

- Can I use the cash value from a permanent life insurance policy while I’m alive?

Yes, permanent policies like whole or universal life accumulate cash value over time, which you can access through loans or withdrawals. This can be used for various financial needs, though loans accrue interest and withdrawals reduce the death benefit.

- How does my credit score affect my life insurance application?

While not a direct factor in premium calculation, like age or health, some insurers may use a credit-based insurance score as part of their underwriting process to assess financial responsibility, which can indirectly influence eligibility or rates.

- What if my health changes after I get a policy? Will my premiums go up?

Once your policy is “in force,” your health status generally won’t cause your existing premiums to increase for that specific policy, unless you try to increase your coverage amount. This is one reason why getting coverage early can be beneficial.

- Is it possible to get a life insurance policy without a medical exam?

Yes, “no-exam” or “simplified issue” policies exist. They typically rely on health questionnaires and database checks instead of a physical exam. While convenient and faster, they often have higher premiums and/or lower coverage limits.

- What if I move to a different state or country after getting my policy?

Generally, your life insurance policy remains valid regardless of where you move within the United States. If moving internationally, it’s best to confirm with your insurer, as some policies may have geographical limitations or require specific notifications.

- How often should I review my life insurance coverage?

It’s wise to review your policy every 3-5 years or after any major life event, such as marriage, divorce, the birth of a child, purchasing a new home, a significant increase in income, or a change in dependents’ needs.

- What are some common reasons a life insurance claim might be denied?

Claims can be denied for reasons like misrepresentation on the application (e.g., not disclosing a pre-existing condition), non-payment of premiums, or death occurring during the “contestability period” (typically the first two years) where the insurer can investigate the application for fraud.

- What’s the “contestability period,” and what does it mean for my policy?

This is a period (usually the first one or two years after policy issuance) during which the insurance company can investigate the accuracy of the information provided in your application. If a claim occurs during this time and material misrepresentations are found, the insurer can deny the claim.

- Should I name a trust as my beneficiary?

Naming a trust as a beneficiary can offer benefits like control over how and when the death benefit is distributed, especially if you have minor children or beneficiaries with special needs. However, legal guidance is required to set it up properly.

- What if I already have some life insurance through my employer? Is that enough?

While employer-provided group life insurance is a good start, it’s often insufficient for most families’ needs (e.g., 1-2 times your annual salary). It’s generally best to supplement it with an individual policy to ensure adequate coverage.

- How can I ensure my beneficiaries know about my life insurance policy and how to claim it?

Keep policy documents in a secure, accessible place and inform your beneficiaries or a trusted advisor/executor about the policy’s existence, the insurer’s name, and how to contact them. Providing a copy of the policy to your executor is also a good idea.

What Are the Different Types of Life Insurance?

The two main types are term life insurance (coverage for a set period, like 10-30 years) and permanent life insurance (lifelong coverage with subtypes like whole or universal life).

Term life insurance is usually cheaper and ideal for temporary needs, like covering a mortgage or raising kids. Permanent life insurance is pricier but builds cash value over time.

Mortgage & Other Specialized Options

For first-time homeowners, decreasing term life insurance (or mortgage life insurance) aligns with a repayment mortgage, reducing coverage as the debt shrinks.

Other options include serious illness coverage for medical costs or income protection if you can’t work. These can often be added as riders to a policy.

| Type | Coverage Period | Cost | Best For |

| Term Life | 5-30 years | Affordable | Young families, mortgage holders |

| Whole Life | Lifetime | Higher | Long-term wealth planning |

| Decreasing Term | Matches mortgage | Low | First-time homeowners |

| Universal Life | Lifetime | Variable | Flexible premium needs |

How Much Life Insurance Do I Need?

A common rule is to get a death benefit equal to 10 times your annual salary, but your needs may vary. Use a life insurance calculator to factor in debts (e.g., mortgage), living expenses, and future goals (e.g., kids’ education).

For example, a $50,000 salary might suggest $500,000 in coverage, but a $200,000 mortgage could push it higher.

New homeowners should ensure coverage at least matches their mortgage balance. If you have dependents, add enough to replace your income for 5-10 years. A financial planner can refine this, but starting with a calculator is quick and free.

How Much Will Life Insurance Cost?

Premiums depend on age, health, coverage amount, and policy type. Younger buyers (under 35) get lower rates, e.g., a 30-year-old might pay $20-$40/month for a $500,000 term policy.

Smoking, chronic illnesses, or high-risk jobs can raise costs.

No-exam policies are pricier but faster for healthy applicants. Shop early, as premiums rise with age. Compare quotes from at least three insurers, and consider bundling with home or auto insurance for discounts.

Online insurers like Haven Life often have lower rates due to streamlined processes. This table shows sample monthly costs for a $500,000 term policy (20-year term, non-smoker).

| Age | Male | Female |

| 25 | $18-25 | $15-22 |

| 35 | $25-35 | $20-30 |

| 45 | $50-70 | $40-60 |

Tips for First-Time Buyers

Explaining the life insurance application process can feel daunting, especially when you’re juggling major life changes like buying a home or starting a family. Here are detailed tips to make it smoother and avoid common pitfalls, tailored for first-timers:

Plan for Timing

Start the process at least 30-45 days before you need coverage, such as your home closing date or a child’s birth. Underwriting can take weeks, and delays could leave you unprotected. For example, if you’re closing on a house in July 2025, begin shopping in early June to align coverage with your move-in date.

Provide Accurate Mortgage Details

For mortgage-related policies like decreasing term insurance, share your mortgage term (e.g.,15 or 30 years), interest rate, and remaining balance. This ensures coverage matches your debt. If you’re unsure, check your loan documents or ask your lender for a payoff statement to avoid over- or under-insuring.

Be Honest About Health & Lifestyle

Disclose all health conditions, smoking habits, or high-risk activities (e.g., skydiving) during the application. Inaccurate information can lead to denied claims, leaving your family without benefits. If you have a pre-existing condition, like diabetes, consider no-exam policies from insurers like Ethos, which may offer coverage with simpler health reviews.

Choose the Right Application Method

If time is tight, opt for no-exam policies, which skip medical exams and rely on health questionnaires or data like prescription records. These are ideal for healthy applicants but cost 10-20% more. Alternatively, digital platforms like Haven Life use eApps for faster processing (sometimes under a week), reducing paperwork compared to traditional agents.

Work With an Independent Agent

Unlike agents tied to one insurer, independent agents can compare multiple providers to find the best rates and coverage. They can also explain complex terms, like accelerated death benefit riders, and ensure your policy aligns with needs like mortgage protection. Search for licensed agents through platforms like Trusted Choice.

Double-Check Beneficiary Details

Name primary and contingent beneficiaries (e.g., spouse as primary, sibling as contingent) clearly, including full names and Social Security numbers if required. Update these after major life events, like marriage or a child’s birth, to avoid delays in payouts. Some insurers allow online beneficiary updates for convenience.

Avoid Overloading on Riders

Riders like child life or disability coverage can enhance a policy but increase premiums. As a first-timer, stick to essentials such as a terminal illness rider if you’re concerned about medical costs to keep costs manageable. Discuss rider benefits and limitations with your agent to avoid surprises, like taxable payouts.

Keep Records Organized

Save copies of your application, policy documents, and correspondence with the insurer. Use digital tools like Evernote or a secure cloud folder to track everything. This helps if you need to reference terms or resolve issues, especially during underwriting or claims.

Common Struggles and Solutions for First-Time Buyers

Lack of Transparency

Issue: Hidden fees or unclear terms confuse buyers.

For example, some don’t realize accelerated death benefits (early payouts for terminal illness) may be taxable or reduce the death benefit.

Solution: Choose reputable insurers with high customer satisfaction (check J.D. Power or Google Reviews). Read policy terms or ask agents to explain riders like accelerated death benefits.

Slow & Paper-Heavy Processes

Issue: Manual, paper-based applications take weeks, frustrating buyers who need quick coverage (e.g., before a home closing).

Solution: Opt for insurers using digital tools like eApps or platforms like PaperClip’s Mojo, which digitize paper forms for faster processing. No-exam policies also speed things up.

Not Understanding Policy Limitations

Issue: Buyers are surprised by exclusions, like no coverage for self-inflicted injuries in accelerated death benefits.

Solution: Review exclusions with your agent.

For example, confirm if terminal illness riders cover your needs or if mortgage life insurance suits a repayment mortgage.

Feeling Overwhelmed by Choices

Issue: Too many policy types and riders overwhelm first-timers, leading to decision paralysis.

Solution: Focus on term life for affordability or decreasing the term for mortgages. Use online calculators and limit riders to essentials (e.g., child life or disability).

| Common Struggles | Solution |

| Lack of Transparency | Choose reputable insurers, review terms |

| Slow, Paper-Based Processes | Use digital eApps, no-exam policies |

| Policy Limitations | Clarify exclusions with the agent |

| Too Many Choices | Focus on term life, limit riders |

Wrapping Up Your Life Insurance FAQ Journey

We’ve made it super simple, life insurance isn’t just something grown-ups buy. It’s a big way to take care of your family. If you’re buying a home for the first time, it’s like a strong bridge that keeps your family safe if something happens to you.

Now you know about the different kinds, how much you might need, and how to avoid mistakes. You’re ready to pick what’s best! Go ahead and do it, and you’ll feel great knowing your family is protected.