Credit cards raise many practical questions, even among financially experienced users and professionals. From APR structures and credit limits to transaction fees, reward systems, and credit reporting, multiple factors shape how credit cards function within the broader financial ecosystem.

As digital payments expand and credit scoring models evolve, understanding how these elements influence borrowing costs, spending behavior, and credit history becomes increasingly important. This blog answers common credit card questions to clarify how eligibility rules, charges, rewards programs, and usage practices work together in modern consumer finance—structured in a way similar to Yonyx Interactive Decision Trees to break down complex concepts step-by-step.

Summary

- Clear explanations of essential credit card concepts, including eligibility, APR, balances, minimum payments, and how credit cards work

- Coverage of key credit card charges and costs, such as interest rates, annual fees, transaction fees, and penalty charges

- Insights into rewards programs and benefits, including cash back, points, and strategies for maximizing credit card rewards

- Practical guidance on responsible credit card usage, credit score impact, debt management, and ways to avoid interest and overspending

Credit Card Basics & Core Concepts

1. How does a credit card work?

A credit card is a revolving line of credit that lets you borrow money from a bank to make purchases up to a credit limit. If you pay the full balance during the grace period, you avoid interest. Otherwise, the remaining balance accrues APR interest, while timely payments help build your credit history.

2. What is APR in credit card?

APR (Annual Percentage Rate) is the yearly cost of borrowing on a credit card, expressed as a percentage. It determines the interest charged if you carry a balance past the due date. Paying the full statement balance each month usually avoids APR charges and helps manage credit card costs.

3. What is a good APR for a credit card?

A good credit card APR is typically below the national average of about 21%–22%. Excellent credit may qualify for 13%–18% APR, while rates above 24% are considered high. The exact APR depends on your credit score, card type, and lender terms, with higher scores usually receiving lower interest rates.

4. What is CVV in credit card?

CVV (Card Verification Value) is a 3- or 4-digit security code on a credit or debit card used to verify online or phone transactions. It helps prevent fraud by confirming the user has the physical card. On Visa, Mastercard, and Discover, it appears on the back, while American Express displays it on the front.

5. What is minimum due in credit card?

The minimum payment on a credit card is the smallest amount you must pay by the due date to keep your account in good standing and avoid late fees. It is usually 1% to 4%of the balance or a fixed amount, but paying only the minimum leads to interest charges and longer debt repayment.

6. What is the difference between a charge card and a credit card?

A charge card requires the full balance to be paid each month and usually has no preset spending limit. A credit card offers revolving credit, allowing you to carry a balance and pay a minimum payment, but it charges APR interest and has a defined credit limit.

7. What does current balance mean on a credit card?

The current balance on a credit card is the real-time amount you owe, including posted purchases, payments, and pending transactions since the last billing cycle. Unlike the statement balance, it updates continuously and affects your available credit and spending capacity.

Eligibility, Application & Account Management

8. How to cancel a credit card?

To close a credit card, first pay off the balance, redeem rewards, and cancel automatic payments. Then contact the card issuer to request closure and destroy the card. Finally, check your credit report to confirm the account is marked closed, as closing a card may impact your credit score.

9. How old do you have to be to get a credit card?

In the U.S., you must be at least 18 years old to apply for a credit card. Applicants aged 18–20 must show independent income or have a co-signer, while those 21 or older can apply without income proof. Some banks also allow younger individuals to be added as authorized users.

10. How long does it take to get a credit card?

After credit card approval, most issuers deliver the physical card within 7 to 10 business days by mail. Some banks provide instant digital card access for online purchases, while expedited shipping (1 to 2 days) may be available for faster delivery, depending on the issuer.

Usage & Transactions

11. Can you pay rent with a credit card?

Yes, you can pay rent with a credit card through landlord portals or third-party services. Most charge 2.5% to 3% processing fees, which may exceed rewards earned. Paying rent by credit card can build credit history, but high balances may increase credit utilization and lead to interest if not paid in full.

12. How to use credit card?

Use a credit card for in-store or online purchases, then pay the full statement balance each month to avoid interest. Keep credit utilization below 30%, pay on time, and monitor transactions regularly. Responsible credit card use helps build credit history, avoid debt, and maximize rewards like cash back or points.

13. Can you pay taxes with a credit card?

Yes, you can pay taxes with a credit card through IRS-authorized payment processors, but they charge processing fees of about 1.75% to 2.35%. While this option may earn credit card rewards, the fees and potential APR interest can outweigh the benefits if the balance is not paid in full.

14. Can you buy gift cards with a credit card?

Yes, you can buy gift cards with a credit card at many retailers, supermarkets, and online stores. However, some issuers may treat certain prepaid gift cards as a cash advance, which can trigger fees and interest. Rewards eligibility and purchase limits may also vary by card issuer.

15. Can I buy a car with a credit card?

Yes, you can pay for a car with a credit card, but most dealerships allow it only for a down payment or partial payment, often capped at $3,000 to $5,000 due to 1% to 3% processing fees. Always confirm the dealer’s policy and consider the credit limit and APR before using a card.

16. How to take money from credit card?

You can withdraw money from a credit card through a cash advance at an ATM, bank teller, or by using convenience checks. Cash advances usually have lower limits, 3% to 5% fees, and high APR interest that starts immediately, making them an expensive option for borrowing cash.

Costs, Fees & Interest Management

17. Why is it important to find a credit card with a lower APR?

Choosing a low APR credit card reduces interest charges when carrying a balance, allowing more of each payment to go toward the principal. This lowers monthly costs, speeds up debt repayment, and improves financial flexibility. A lower credit card APR is especially useful for large purchases or balance transfers.

18. Which of the four factors directly impact your total cost of using the credit card?

- Annual Fee: The yearly cost for card membership.

- APR: The interest charged on carried balances.

- Penalty Fees: Costs for late or returned payments.

- Grace Period: The window to pay without interest.

19. How to avoid interest on credit card?

To avoid credit card interest, pay the full statement balance by the due date each month during the grace period. Avoid cash advances, which charge interest immediately, and consider 0% APR promotional offers for large purchases if you can repay the balance before the promotional period ends.

Credit Score & Financial Impact

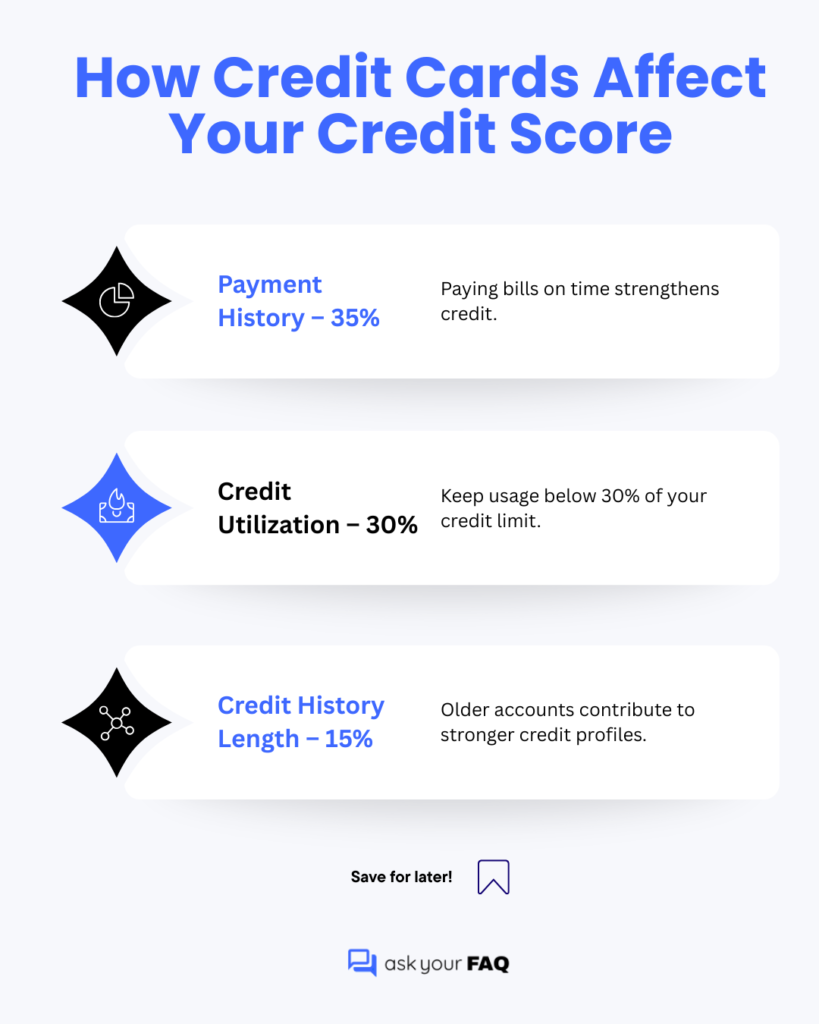

20. Which type of card impacts your credit history?

Credit cards, such as student credit cards, secured credit cards, and unsecured credit cards, affect your credit history because issuers report payment activity to credit bureaus. Your payment history, credit utilization, and new credit inquiries influence your credit score. Debit cards or IDs do not impact credit history.

21. What is the advantage of paying your credit card balance in full each month?

Paying your credit card balance in full each month avoids high APR interest and late fees, keeps your credit utilization low, and improves your credit score. It also builds a positive payment history and prevents debt from growing, making it easier to maintain strong long-term financial health.

22. How to build credit without a credit card?

You can build credit without a credit card by reporting rent and utility payments, using credit-builder loans, or services like Experian Boost. Becoming an authorized user on someone else’s card and making on-time loan payments also builds a positive credit history with major credit bureaus.

23. Does closing a credit card hurt your credit?

Yes, closing a credit card can hurt your credit score because it reduces your total available credit and may increase your credit utilization ratio. It can also shorten your average credit history, especially if the account is old or has a high limit.

Rewards, Benefits & Spending Behavior

24. Can you get cash back with a credit card?

Yes, you can get cash back from a credit card through cash back rewards, where cards return 1% to 5% on purchases. Some cards also allow cash advances at ATMs, but these involve high fees and immediate APR interest, making rewards-based cash back the better option.

25. What are all the ways you spend more money when you pay with a credit card?

Credit cards can increase spending because digital payments reduce the pain of paying, making purchases feel less tangible than cash. Easy transactions encourage impulse buying, higher transaction amounts, and overspending. Carrying balances also adds high APR interest and fees, increasing the total cost of purchases.

Industry & Business Model Insights

26. What are at least two ways credit card companies make money?

Credit card companies make money mainly through interest charges (APR) on unpaid balances and interchange fees paid by merchants on each transaction. They also earn revenue from annual fees, late payment fees, and balance transfer fees, even when cardholders avoid interest by paying their balance in full.

27. What are some of the common marketing tactics credit card companies use to market to young adults?

Credit card companies target young adults through social media marketing, influencer partnerships, and sign-up bonuses. They promote cash back rewards for dining, streaming, and travel, along with starter or secured credit cards. Many also use mobile apps, gamified budgeting tools, and personalized offers to build early brand loyalty.

Credit Card Essentials: What to Remember

Credit cards combine convenience, purchasing power, and credit-building potential, but they also involve interest rates, fees, and usage rules that influence financial outcomes. Understanding how eligibility, APR, rewards, and credit reporting interact allows users to evaluate cards more strategically.

By addressing common questions on costs, benefits, and responsible usage, this guide provides a clear overview to support informed decisions and better long-term credit management.